Intrinsic value can be thought of as the true value of something rather than the cost of something.

Let me explain WHAT exactly that is before we get into HOW to find it.

Imagine you find yourself at a thrift store trying on a pair of used jeans and they have a $10 price tag.

They are currently ‘worth’ $10 to anyone that looks or thinks about buying them, that is their cost.

You try the jeans on, they fit PERFECTLY, but theres a hole in the left pocket. That isn’t good. As the potential owner of the jeans, that hole could lead to you losing or misplacing items in the future. It is important you know it is there.

Since you DO know its there, you know the jeans are not worth $10 as advertised. Instead, there’re worth only $9, which would be the value. We want a discount because we can either accept the hole as a hole and live with it or fix the hole at your own cost. Regardless of our decision, the hole is still there.

Now we are slightly nervous about the integrity of the rest of the jeans, and perhaps even begin to have distrust in the store. So we do a very thorough check of all the pockets and zippers so we can feel comfortable with our purchase.

Upon a check of every pocket and zipper, we find a $5 bill crumpled and tucked away in one of the zippers. Jackpot! The catch is you can’t take it without first buying the jeans.

So what is the intrinsic value of these jeans?

Jeans worth: $10

Hole in the pocket: -$1

Cash in the pocket: $5

We determine the intrinsic value to be $14.

Knowing what we know now, we can comfortably buy the jeans for $10 since we are getting $14 ‘worth’ of value in return. A 40% return, or inversely a 28% discount.

However, what you should do is get your $1 discount for the hole in the jeans anyways. The hole hasn’t gone away with the discovery of the cash. Knowing they are worth $14; we pay $9 to take them home. A 55% return, or inversely, a 35% discount.

Something you may be thinking “wouldn’t that be immoral?” My answer is no! The seller lists the price. It’s not up to the buyer to overpay due to the store’s negligence to check the pockets, or to ask to pay more due to the ignorance of the seller. Just like stocks, we never care WHO we are buying our stocks from, only that we are getting the best possible deal for ourselves. Every time you buy, someone sold. Every time you sell, someone bought. In each instance only one of these two people is right, but both believe it to be themselves.

It’s not up to the buyer to overpay for the sellers ignorance

Also note that a $1 discount, paying $9 instead of $10 increased our return by 38% even though the jeans were worth the same in both instances. This is why the purchase price is extremely important when investing. You do not want to pay just any old price; you want to pay the RIGHT price.

Warren Buffett knows this, and he knows this in part thanks to Benjamin Graham. Graham is the author of a pair of must-read books; "Security Analysis" (1934) and "The Intelligent Investor" (1949).” He also is attributed to pioneering security analysis & value investing as a whole. If this is the first you are hearing of Ben Graham, and are truly interested in investing I definitely recommend going down the rabbit hole and reading his books.

Since we aren’t particularly interested in investing in Jeans? How do we calculate the intrinsic value of a stock? Well, here’s is Ben’s answer:

At face value, this looks so confusing maybe we would rather just invest in used jeans... but I promise it is not. Here is how to read this formula

V= Intrinsic Value, we are solving for VEPS= Current EPS TTM (earnings per share)8.5= The P/E of a non-growth company, Ben used 8.52g= Where ‘g’ is 5Y-10Y earnings growth estimates4.4= Avg yield of high-grade corporate bonds ( 20Y / 1962)Y= Current yield on AAA corporate bonds

Knowing what the variables mean, we just need to fill in the blanks.

EPS (TTM) can be found on Yahoo Finance, Seeking Alpha, Finviz, and other similar sites.

8.5 P/E represents “no growth” so if 8.5 seems expensive for no growth, feel free to adjust this down. Keep it within 7.0 and 8.5, otherwise, the formula loses integrity.

“2 x g” where G = EPS growth has worked well for quite some time, but today where Tesla and Amazon are companies that exist, multiplying growth by 2x can be aggressive. To combat this many adjust “2 x g” to just “g.” We always want to err on the side of caution so using ‘worst case’ in many ways should be your ‘base case’ for exploring new ideas. Bake in a margin of safety.

Lastly, for ‘Y’ we will want to use long term AAA corporate bonds (found here). Current yields are ~1.60% with a long term average of 4.18%. With such a wide discrepancy it’s wise to use the metric with the longer track record, or whichever is more conservative. Since ‘Y’ is the denominator of the equation we will use the higher 4.18% for example purposes.

Using this information let’s ‘modernize’ the intrinsic value formula

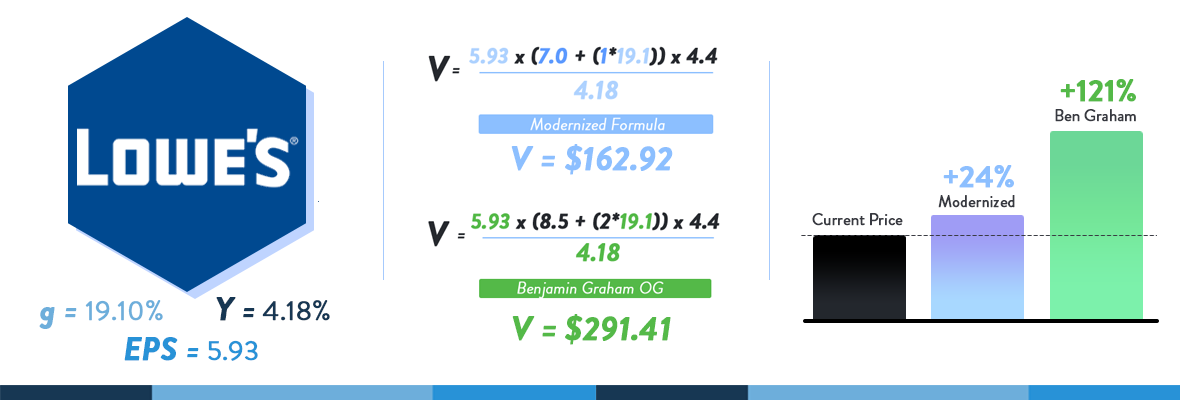

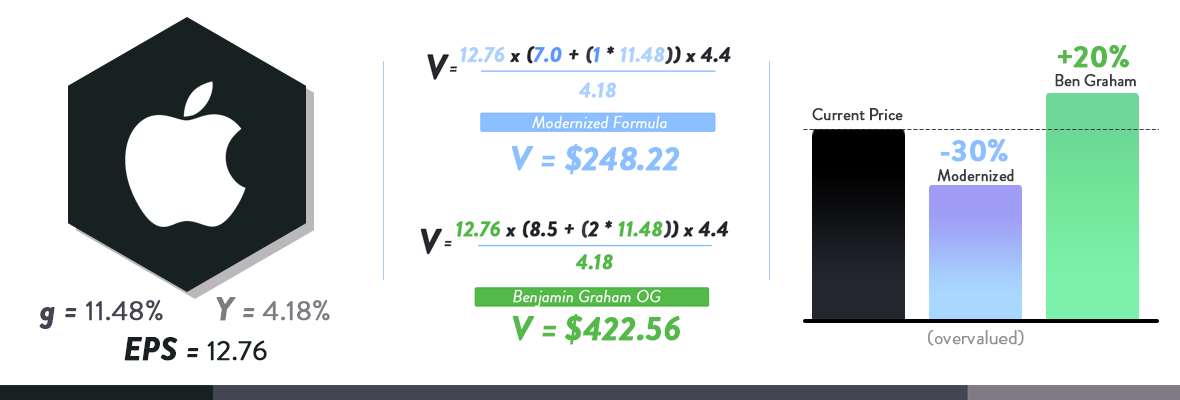

Let’s take both formulas on a test drive with some examples:

Using the information from above, let’s determine the intrinsic value of some popular names on the market & some that appear to be attractively valued.

Note: Tesla EPS is -$0.87 at the time of writing this, I have used +$0.87 since the formula doesn’t work with negative earnings. This means EPS listed is +200% greater than reality and technically would count towards one of the 5Y of EPS growth. This process results in an inflated intrinsic value. Sorry Elon.

Now that we have learned to figure out what a stock is worth (its intrinsic value, not its price) we can begin to put together a watchlist to track our stocks. This allows us to take action if a specific stock price drops below the range that we deemed its ‘Intrinsic Value’ to be; almost like a buy signal. In doing so, we can purchase shares with confidence. Similar to our scenario with the used Jeans, we know we got a good deal!

So, are we done? Not quite.

Lastly, we add in our margin of safety, since investing is hard

A margin of safety could also be called insurance. If we determine the intrinsic value of a stock to be $100, and its currently trading at $115, should we buy once it drops back down to $100?

The answer should be NO!

Why? If a stock is worth $100, and we pay $100, we are paying full price even though it dropped $15 to arrive there. That $15 drop is not a discount, its an overpriced stock returning to its true value. What we want to do is what Buffett does, which of course he learned from Graham.

Following this theory, Buffett would look to buy a stock worth $100/ share at $90/share. That way if he is wrong about the stock being worth $100, he has a risk cushion. If he is right about the stock, he bought a dollar bill for 90 cents.

It’s also important to understand that the market doesn’t always get it right. We can see that due to the fact that the stock was trading at $115, despite it only being worth $100. Inversely stocks can be sold below its intrinsic value. It’s this separation between value and price that creates opportunities in the market.

What margin of safety you choose is up to you. The higher the % the fewer opportunities you will find. The lower the % the riskier your investments become. Common safety margins are 10%, 25%, and 50% (50% for those who want to buy 1 stock every 4 years, trust me these are not common).

Benjamin Graham’s intrinsic value method & a modern formula to use for today’s investing environment. Intrinsic value is a great tool to guide your investment strategy & plan. However it’s very important to understand that intrinsic value is not owed to you, you may never see that price. Not only that, but there is also nothing to say your calculations are correct, so never use this as your only prerequisite to an investment. Instead, use this as a supporting argument for your thesis.

Ben Graham’s intrinsic value method was created with value investing in mind. There are many variables that affect a stock price outside of our calculation inputs. As an investor, you must soak all information (good and bad) when making decisions. Never rely solely on one method, and never get too comfortable. Value investing may seem easy, but it is not. It takes plenty of practice and even more patience. If you don’t believe me, perhaps old Charlie Munger can better explain.

Between my investment page and this newsletter, I sink a LOT of time into FREE content for you all. If you found this article useful at all, please support this page by dropping a follow & leaving a like and a comment! More content will follow, so stay tuned.

You can support & give back by signing up for the newsletter and sharing this article with a friend that bought hertz or went all-in on tesla at 1k😭.

I appreciate you all. Until next time,

Ryan, SDW Investing

Ryan, phenomenal job. You break down concepts that might be simple but are definitely hard to put in practice which is a skill of its own. If you could breakdown (maybe over multiple weeks) your investment process/routine, I'd be very grateful. That would help everyone here (including myself) that might be inexperienced in the world of investing a foundation of things to look at and perhaps give us training wheels for building a process of our own.

Very detailed, good explanations of the metrics and valuable information. 10/10